How to use sector diversification to manage risk

Portfolio diversification is a subject that divides opinion, and it’s one that most investors approach by thinking in terms of numbers. It ends up being a balancing act between offsetting the risk of single failures against the costs and effort of managing dozens of positions. On this point, even the pros have differing views. Small-cap fund manager Giles Hargreave is content with over 200 hundred holdings, while the likes of Schroders’ Nick Kirrage is more than happy with 40, and even less.

But there’s more to diversification than looking for safety in numbers. Being aware of how resilient a company is to the broader economy is important in managing exposure and smoothing returns over time.

Understanding sector sensitivity

All stock market data services categorise companies based on the sector they fall into. At the top level, there are three super-sectors: Cyclicals, Defensives and Sensitives, and then 10 sectors that are divided between them.

Broadly speaking, Cyclical sectors are those most sensitive to macro trends and the general health of the economy and consumer sentiment. Among them are mining stocks, high street retailers and banks. Defensives, on the other hand, are seen to be less reliant on the economy because they sell goods that we buy in good times and bad. They include pharmaceutical companies and utility groups. In between are the Sensitives, which move with the economy but to a lesser extent than Cyclicals.

One distinction between Cyclicals and Defensives can be seen in something called Beta. Beta is a measure of the sensitivity of a company’s share price to the movement of the market (usually over the past five years). If a stock’s price tends to rise more than the market on up-days and fall more than the market on down days, it will have a Beta greater than 1. But if it isn’t as sensitive to market movements, rising less and falling less than the market, then it will have a Beta of less than 1. Very generally, Defensive stocks have lower Betas than Cyclicals because they are less sensitive to market volatility.

Overlooking sector diversification can be costly, as recent periods of market history have shown us.

In the immediate aftermath of the 2008 financial crisis, Defensives generally outperformed Cyclicals because investors plumped for the perceived safe havens of companies that were resilient to unsettled economic conditions. More recently, the uncertainty caused by the EU referendum in 2016 was a classic example of how Cyclicals and Defensives perform differently when the mood of the market changes. Stocks with strong ties to the UK economy, particularly housebuilders and retailers were marked down, while more defensive plays in pharmaceuticals and consumer goods shot up.

Taking action on diversification

Without knowing the future, these differing views reinforce the importance of diversifying between sectors. That way, an “all weather” portfolio should always have some exposure to sectors that are on the up.

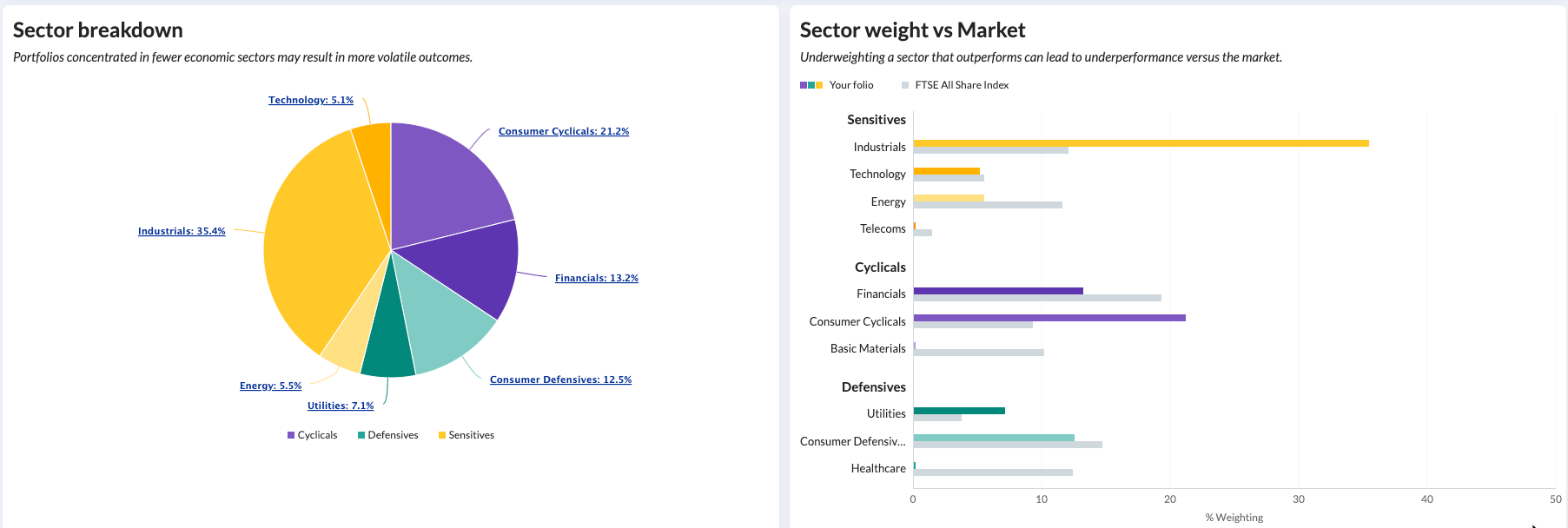

You can use the Sector Breakdown charts in the Allocation tab of the Folios tool to assess your own portfolio's sector exposure and also its weight versus the benchmark.

This latter point is important because if you are significantly overweight in a sector that subsequently underperforms, then you will have a headwind relative to benchmark. If you have similar weights to benchmark then you might limit your relative sector bets, meaning the specific performance of the stocks you pick will have more of an impact on your performance relative to the benchmark than your sector weighting.

On the other hand, you may not want your sector to look exactly like the benchmark and instead you might seek to make active bets. Active differences don’t guarantee outperformance versus the benchmark, but more structuring your portfolio this way is more likely to generate a variation in performance.

The important thing when you are analysing your portfolio is that you aware of your sector exposures and impact they can have on your returns in different market environments.